")

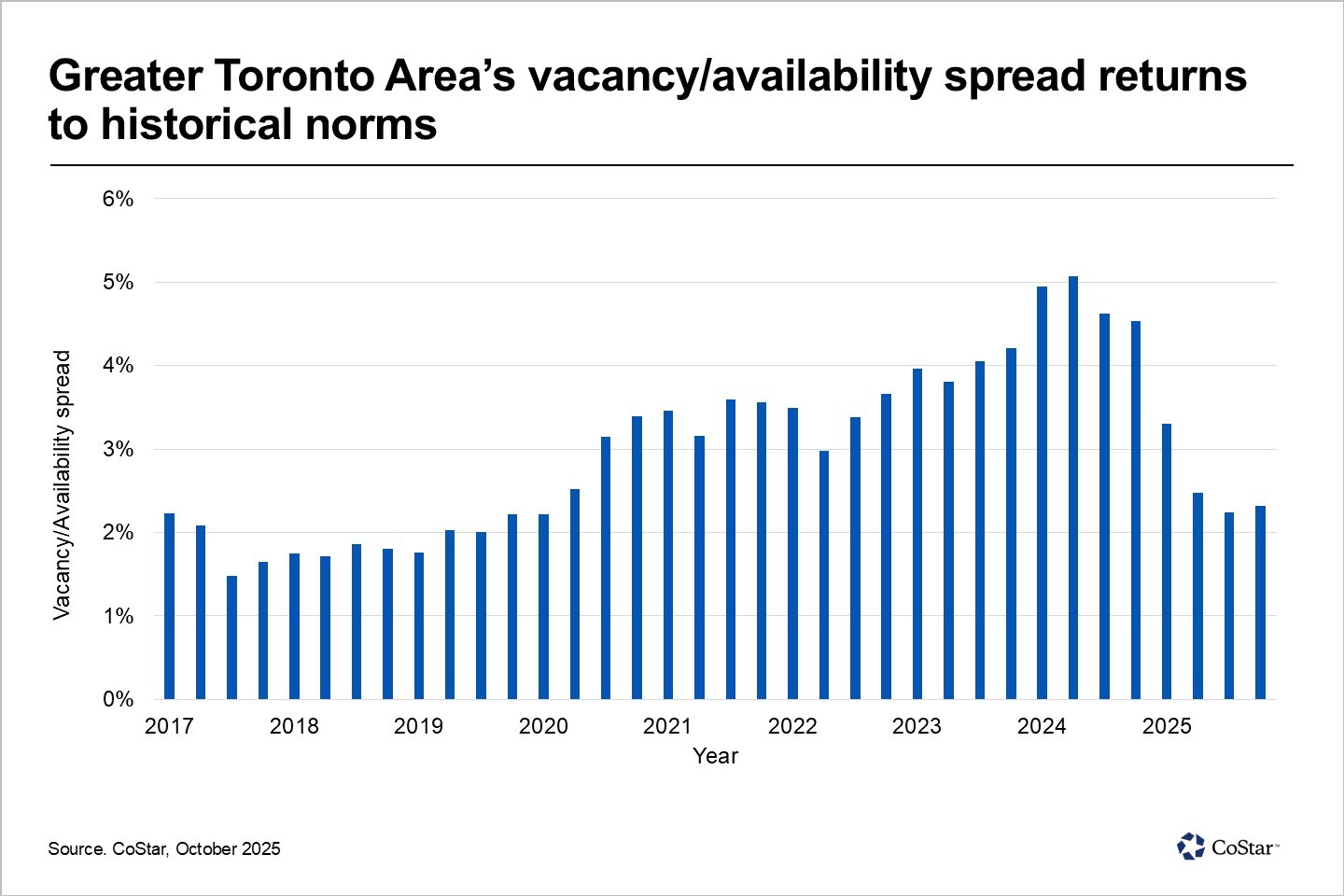

The Gap Between The Vacancy And Availability Rates In Toronto’s Office Market Has Narrowed Back To Pre-covid Averages, A Promising Sign Of Stabilization.

While similar, the two metrics differ slightly and the gap between them can be used to gauge the trajectory of the leasing market. Vacancy refers to office space that is unoccupied and not generating income, whereas availability includes vacant space as well as office space that may still be occupied but is currently being marketed as available, such as the space occupied by a tenant that is not renewing its lease.

Both metrics remain elevated, with vacancy currently 357 basis points higher than the 10-year trailing average and availability ahead by 298 basis points. However, the shrinking size of the gap between the two suggests that the office market is no longer deteriorating and is instead beginning to recalibrate.

If the office sector were a hospital patient, this would be the moment they’re moved from intensive care to the general ward: still under observation, but no longer in critical condition.

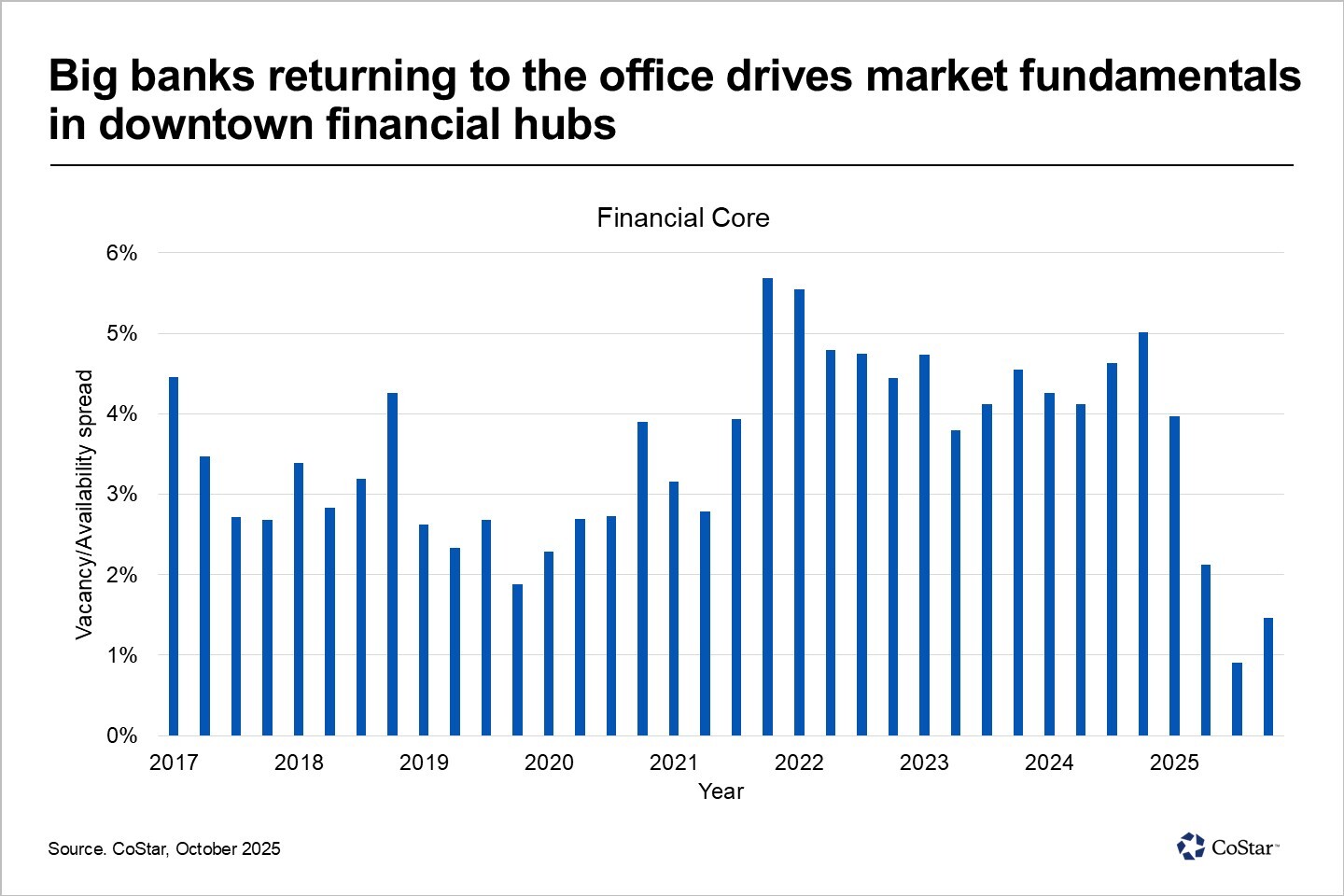

However, this initial recovery is not evenly distributed. The financial core area of downtown Toronto has led the rebound, with the vacancy-availability gap dropping below 1% in the third quarter, its tightest spread in over a decade, compared to a 10-year trailing average of 3.8%. As of mid-October, the gap remains at 1%. This reflects strong tenant retention and fewer subletting listings in prime downtown office buildings. In fact, sublet space now accounts for 17.3% of all available space in downtown submarkets, having peaked at the end of 2022 at 27.8%.

Conversely, suburban office submarkets continue to lag. While the divide between vacancy and availability is narrowing, it remains above historical norms, indicating slower absorption, the net change in occupancy, and more cautious leasing behaviour. Nonetheless, the trend is clear; even these areas are seeing a gradual narrowing of the gap.

Toronto’s office market is undergoing what some of have called a ‘K-shaped’ recovery. Leasing performance is strengthening in the downtown core area, but value erosion through capitalization rate expansion may offset comparative gains when compared to suburban office buildings. For office landlords and investors, the most important metric, asset value, remains under pressure, even as occupancy metrics improve.

Source CoStar. Click here for the full story.